The open interest-weighted funding rate for Bitcoin perpetual futures turned negative within the last 24 hours. A negative funding rate typically indicates a bearish mood in the futures market; however, most of the liquidations observed over the past day were on short positions, which often follow price surges.

This seeming contradiction becomes clearer when examining market trends from the previous week. The funding rate in perpetual futures contracts facilitates periodic payments between long and short position holders, helping to align the contract price with the spot price.

A negative funding rate, as seen on March 25 and March 26, indicates that shorts are compensating longs, implying that the contract price is below the spot price — a classic sign of bearish sentiment where traders predict a price decline. On March 25, the funding rate fell to -0.040% and maintained this level throughout March 26, according to data.

Nonetheless, the liquidation data presents a different narrative. Within a single hour, short liquidations amounted to $14.19 million, compared to a mere $671,540 for longs. Over a four-hour span, shorts experienced $23.50 million in liquidations against $2.28 million for longs. Such short liquidations occur when the price rises, compelling short traders to repurchase contracts at elevated prices to cover their positions, which often exacerbates the upward price movement.

How can a negative funding rate, typically signifying bearish sentiment, coincide with predominately short liquidations that imply a price rise? To clarify this, we look at Bitcoin’s spot price movement over the last week.

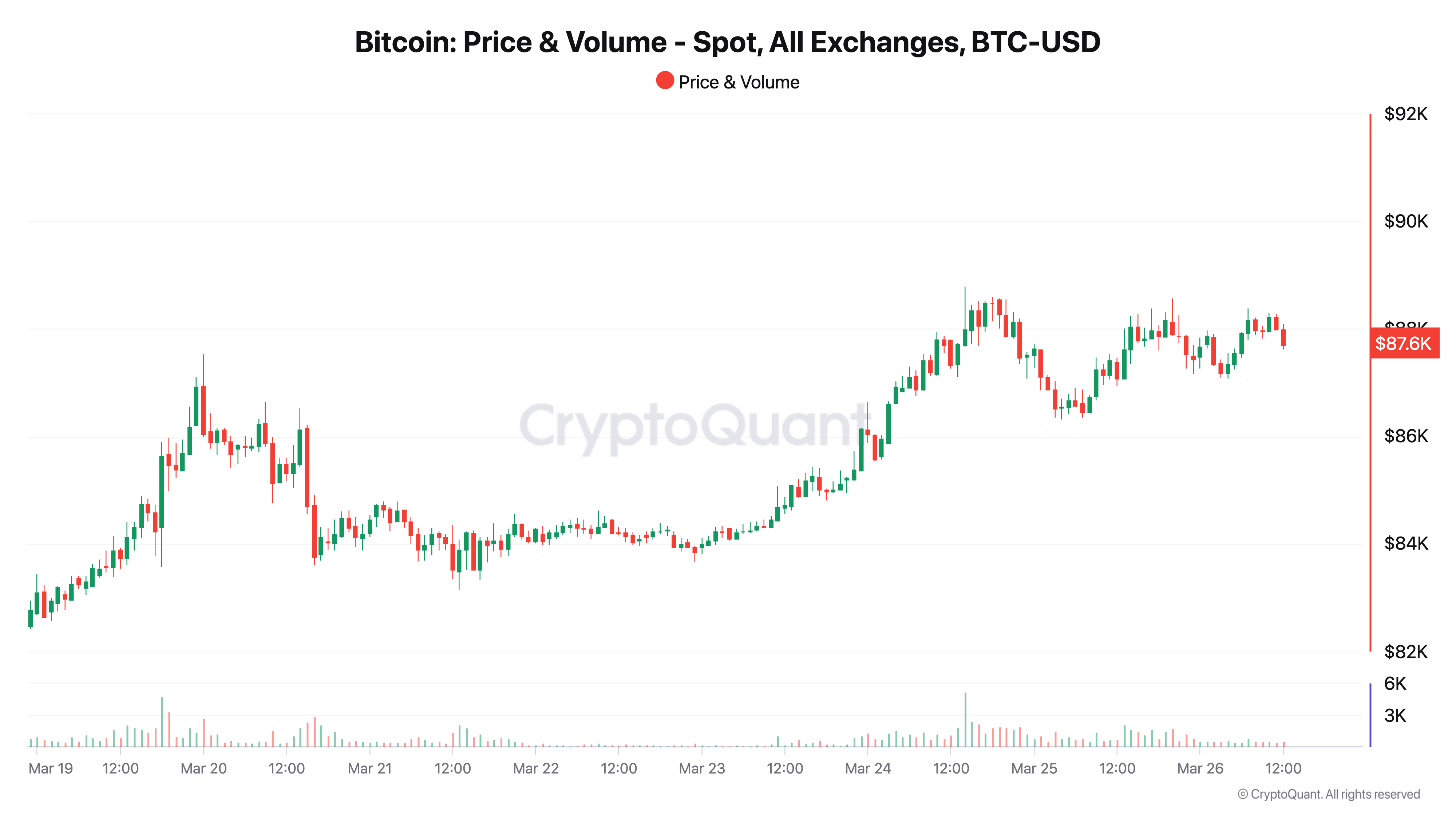

On March 20, Bitcoin closed at $84,175.02. The price saw a slight dip to $84,053.96 on March 21 and further declined to $83,843.18 on March 22. Still, it initiated a consistent climb thereafter, reaching $86,142.15 on March 23 and $87,512.12 on March 24.

This upward trend, representing nearly a 4% increase from March 20 to March 24, was coupled with a positive funding rate, peaking at 0.050% on March 24. A positive funding rate indicates that longs compensate shorts, reflecting a contract price surpassing the spot price, which aligns with the bullish price movement and infers that traders were inclined to pay a premium to maintain long positions.

The pivotal moment occurred on March 25, when Bitcoin opened at $87,515.76, slightly above the previous day’s close, and achieved a peak of $88,564.14, sustaining the upward momentum. However, the price retracted to close at $87,424.41, a modest dip of $87.71 from March 24.

On March 26, Bitcoin opened at $87,488.28, fell to a low of $87,075.71, but surged to close at $88,016.46 — gaining $592.05 since the previous day’s close. This price activity confirms a rally—albeit with some consolidation—that would have triggered the significant short liquidations noted. This indicates that short traders, betting on a price drop, were caught off balance by the rising trend, resulting in a short squeeze that forced them to repurchase contracts at higher prices.

However, the negative funding rate during this period indicates that, on average, the futures market remained bearish. The funding rate is calculated over fixed intervals, often every eight hours, based on the average discrepancy between contract and spot prices. Although the intraday price surges on March 25 and March 26 triggered short liquidations, the average contract price over the funding periods likely remained below the spot price, reflecting an overarching expectation of a price correction. This sentiment may have arisen from the price surge over the past week, leading traders to perceive the market as overbought as prices climbed.

On March 25, Bitcoin’s price fluctuated between a low of $86,322.37 and a high of $88,564.14 — a $2,241.77 swing. This volatility likely contributed to the disconnect between the funding rate and liquidations. The short liquidations were a reaction to the intraday rally, particularly the surge toward $88,564.14. However, the following pullback to $87,424.41 on March 25 and the drop to $87,075.71 on March 26 may have dragged the average contract price below the spot price, leading to a negative funding rate.

This scenario highlights the timing mismatch between funding rate assessments and immediate market movements. While liquidations happen swiftly in response to price fluctuations, the funding rate denotes a longer-term average, capturing the prevailing sentiment throughout the funding period.