Even with Bitcoin’s 2.2% rise on April 1, the cryptocurrency has not traded above $89,000 since March 7. Although the recent price hurdles are often attributed to the intensifying global trade war influenced by the U.S., there were multiple factors affecting investor confidence well before tariffs were announced by President Trump.

Some market observers have suggested that the $5.25 billion in Bitcoin purchases made since February is the main reason BTC has remained above the $80,000 support level. However, irrespective of who is buying, the fact remains that Bitcoin was exhibiting limited upside prior to the implementation of the 10% tariffs on Chinese imports announced on January 21.

Gold/USD (left) vs. Bitcoin/USD (right).

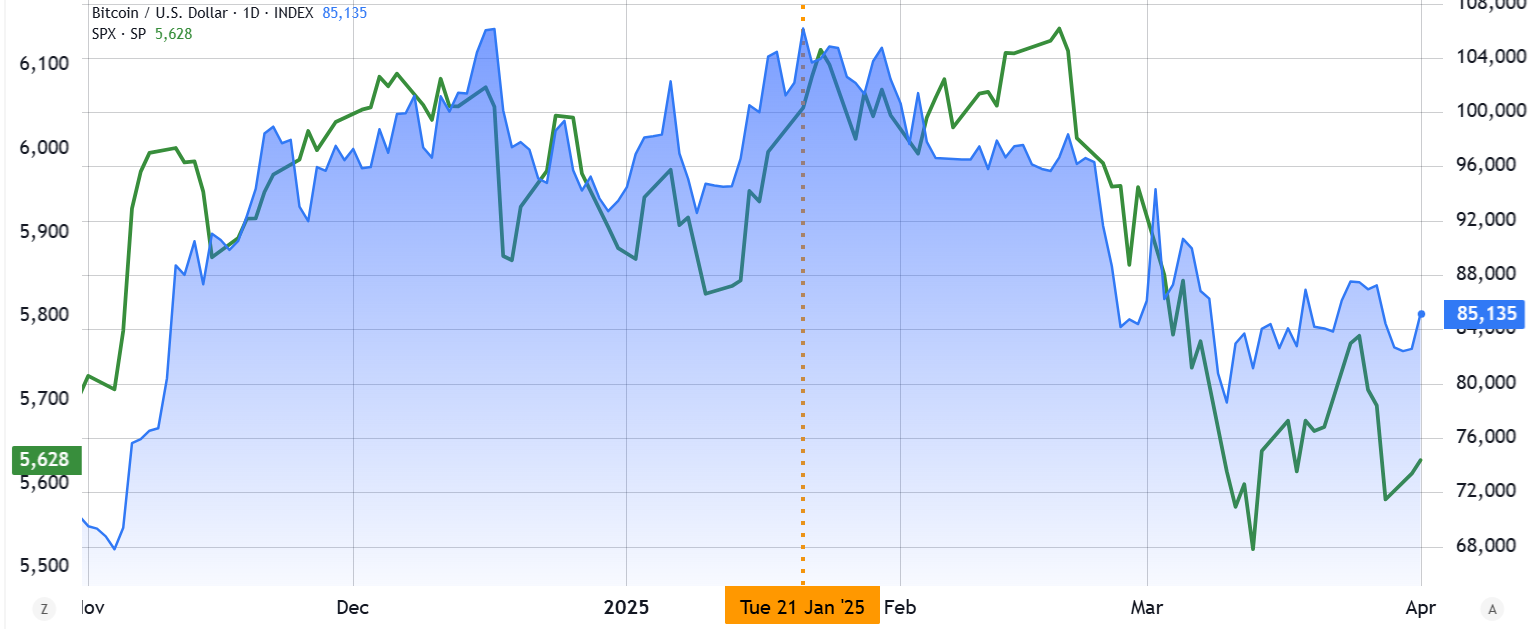

The S&P 500 reached a record high on February 19, precisely 30 days after the trade conflict began, while Bitcoin struggled to stay above $100,000 for the prior three months. It’s clear that while the trade war affected the appetite for risk among investors, substantial evidence indicates that Bitcoin’s price struggles began long before Trump took office on January 20.

Spot Bitcoin ETFs, strategic reserve expectations, and inflation trends

Another aspect that diminishes the connection with tariffs is the spot Bitcoin exchange-traded funds (ETFs), which experienced $2.75 billion in net inflows in the three weeks following January 21. By February 18, the U.S. had announced new tariffs on imports from Canada and Mexico, while both the EU and China had already retaliated. This indicates that institutional interest in Bitcoin remained strong even as the trade war intensified.

Traders’ disappointment after January 21 can also be traced to inflated expectations regarding President Trump’s campaign promise of a “strategic national Bitcoin stockpile,” which was brought up during the Bitcoin Conference in July 2024. As frustration grew among investors, it reached a peak with the issuance of the actual executive order on March 6.

A significant element fueling Bitcoin’s inability to surpass $89,000 is a prevailing inflation trend, reflecting a cautiously effective strategy by global central banks. In February, the U.S. Personal Consumption Expenditures (PCE) Price Index rose by 2.5% year-over-year, while the eurozone Consumer Price Index (CPI) saw a 2.2% increase in March.

Increased risk aversion in light of weak job market data

During the latter half of 2022, Bitcoin’s upward momentum was propelled by inflation exceeding 5%, indicating that businesses and households sought cryptocurrency as a hedge against currency devaluation. Conversely, if inflation remains relatively stable in 2025, lower interest rates would likely benefit the real estate and stock markets more directly than Bitcoin, as reduced financing costs enhance those sectors.

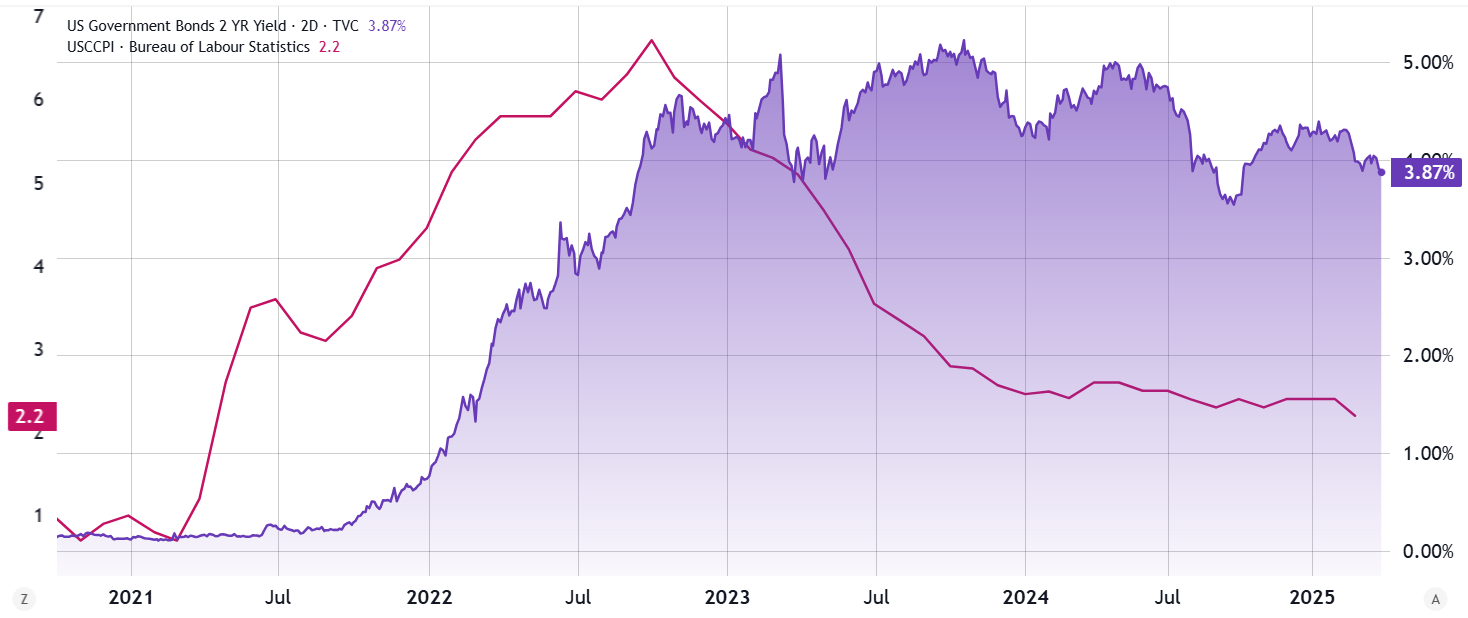

US CPI inflation (left) vs. US 2-year Treasury yield (right).

The weakening job market also diminishes traders’ appetite for riskier assets, including Bitcoin. According to the US Labor Department, job openings fell to a near four-year low in February. Similarly, yields on the US 2-year Treasury dropped to a six-month low, as investors settled for a modest 3.88% return for the security of government-backed bonds. This trend indicates an increasing preference for risk aversion, which is detrimental to Bitcoin’s prospects.

In summary, Bitcoin’s price weakness can be attributed to investors’ unrealistic expectations regarding BTC purchases by the U.S. Treasury, declining inflation that could support potential interest rate cuts, and a more risk-averse macroeconomic climate as investors shift towards short-term government securities. While the trade conflict has introduced negative impacts, Bitcoin was already displaying vulnerability prior to its escalation.

This article is intended for informational purposes and should not be construed as legal or investment advice. The opinions expressed here are solely those of the author and do not necessarily reflect the views of the publication.